On June 24, 2025, Zohran Mamdani—a 34-year-old self-described democratic socialist and state assemblyman from Queens—vaulted into the national spotlight after defeating former Governor Andrew Cuomo in the New York City Democratic primary. His platform centered on a four-year rent freeze for the city’s nearly one million rent-stabilized apartments, extensive public housing development, and tax increases on corporations and high earners. The upset prompted an immediate question for real estate investors: how would markets price this policy risk?

The conventional expectation was straightforward: Mamdani’s proposed rent freeze would directly threaten the revenue streams of landlords with rent-stabilized exposure. Investors in these properties would head for the exits. The Tarin Group tested this hypothesis using an event study of NYC-focused real estate investment trusts (REITs)—publicly traded companies that own and operate income-producing real estate. Because REITs trade on stock exchanges, their prices reflect investors’ collective expectations about the future profitability of the underlying properties. Under this logic, a(n) REIT heavily exposed to NYC apartment buildings, for example, should see its value decline if investors believe rent regulation will materially reduce future rental income.

The results challenge that conventional expectation.

Findings

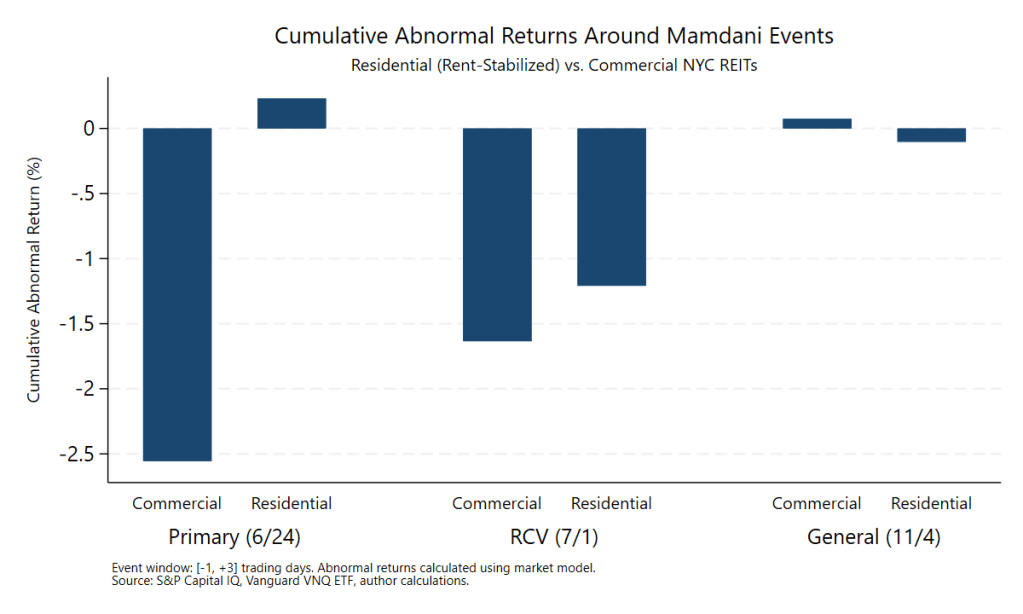

For this study, we analyzed cumulative abnormal returns for eight publicly-traded REITs with significant exposure to NYC real estate around three campaign milestones: the June 24 Democratic primary, the July 1 ranked-choice vote confirmation (RCV), and the November 4 general election. Our sample was split evenly between NYC residential- and commercial-oriented REITs. The residential group—four REITs with NYC portfolios implicated by Mamdani’s proposal—owns apartment buildings and sources revenue from residential rents. The commercial group—four different NYC REITs—owns office and retail properties and generates income from business tenants.

The comparison between these two groups is central to the analysis. If Mamdani’s rent freeze proposal were the primary driver of investor concern, residential REITs—whose revenues depend directly on apartment rents—would have underperformed commercial REITs, whose office and retail tenants are not subject to rent regulation. In other words, residential REITs serve as the “treatment group” directly exposed to the policy proposal, while commercial REITs serve as a “control group,” operating in the same local market but insulated from the proposed regulation.

What we found was the opposite: around the primary election, commercial REITs underperformed residential REITs by 2.8 percentage points—a statistically significant differential (p = 0.01). Commercial REITs experienced average cumulative abnormal returns of -2.6%, while residential REITs posted +0.2%. The pattern held directionally at the RCV confirmation, with both groups posting declines but commercial REITs again exhibiting relative underperformance. By the general election, the differential had largely disappeared as markets fully priced in Mamdani’s expected victory.

Figure 1: Cumulative Abnormal Returns Around Mamdani Events

Interpretation

The finding suggests that investors view Mamdani’s election as a broader threat to NYC’s commercial real estate ecosystem—not merely a rent-stabilized landlord problem. Several factors may help to explain this:

Policy Scope: Mamdani’s platform extended beyond rent regulation to include tax increases on corporations and high earners, skepticism toward commercial development, and a regulatory posture that raised questions about NYC’s business climate. Commercial tenants—unlike apartment renters—have mobility. A corporate tenant can relocate to a neighboring jurisdiction; those in rent-stabilized apartment buildings generally do not have that same flexibility.

Prior Regulatory Adjustment: New York’s 2019 Housing Stability and Tenant Protection Act already constrained rent-stabilized landlord economics significantly, eliminating vacancy decontrol and limiting renovation pass-throughs. For residential REIT investors, Mamdani’s rent freeze represents incremental tightening within an already-constrained framework. For commercial landlords, his administration introduces a new category of uncertainty.

Demand Stickiness: Residential housing demand is structurally sticky. Rent-stabilized tenants have strong incentives to remain in place regardless of the political environment. Commercial real estate lacks this built-in demand floor.

Connection to Consumer Sentiment Research

This final point connects to a pattern we have documented in prior research on consumer behavior. In our analysis of home furnishing retailers, we found that more AI-driven firms exhibited dramatically lower sensitivity to housing market fluctuations—showing approximately 85% less responsiveness to existing home sales than their traditional counterparts. We attributed this to a “locked-in” effect: post-2020 housing affordability constraints reduced household mobility, which in turn shifted consumer spending patterns toward in-place investment rather than transaction-linked purchases.

The Mamdani findings suggest an analogous dynamic in real estate equity markets. Residential landlords—particularly those with rent-stabilized exposure—may benefit from the same demand inelasticity that insulates certain consumer-facing firms from housing cycle volatility. When policy uncertainty rises, assets tied to mobile demand (commercial tenants, transaction-linked retailers) face greater repricing risk than those tied to sticky demand (rent-stabilized tenants, in-place home investment).

Put differently—the “locked-in” homeowner who renovates rather than relocates has structural parallels to the rent-stabilized tenant who stays put regardless of who holds office. Both represent demand bases that are relatively insensitive to external shocks—and both create downstream implications for the firms and assets that serve them.

Limitations

Our sample includes only eight REITs after excluding one outlier (American Strategic Investment Co.) due to extreme illiquidity and near-zero market beta. With four entities per group, statistical power is limited, although the primary election result still achieves conventional significance thresholds. In addition, our analysis cannot fully disentangle Mamdani-specific policy expectations and broader sentiment shifts affecting NYC real estate. A more comprehensive study would incorporate additional NYC-exposed equities and control for confounding market events.

Conclusion

Investors betting on a “Mamdani discount” for residential landlords may be targeting the wrong asset class. Market behavior suggests that policy risk under a self-described democratic socialist mayor falls more heavily on commercial real estate—where tenant mobility amplifies uncertainty—compared to residential portfolios anchored by sticky, regulation-protected demand. For investors and analysts evaluating NYC real estate exposure, the relevant question may not be which landlords face rent regulation, but rather which landlords serve tenants who can afford to leave.

______________________________________________________________________________

Methodology: Market models estimated using daily close price returns from January – May 2025, with Vanguard Real Estate ETF (VNQ) as benchmark. Event window spans [-1, 3] trading days around each event date. Abnormal returns calculated as actual returns minus model-predicted returns; cumulative abnormal returns summed within event windows. Residential REITs analyzed: Clipper Realty, AvalonBay, Equity Residential, and UDR. Commercial REITs analyzed: SL Green, Vornado, Empire State Realty Trust, and Paramount Group.

Data: S&P Capital IQ (daily close prices), Federal Reserve Economic Data.

Credit to Bryan Berlin for the photo